If you are an entrepreneur, you have probably heard of Net Present Value (NPV) and Internal Rate of Return (IRR) before. You might even have used these financial metrics in the past to value your business or technology, or to help you make financial decisions. But how confident are you that you understand these metrics and know how and when to use them?

If you are an entrepreneur, you have probably heard of Net Present Value (NPV) and Internal Rate of Return (IRR) before. You might even have used these financial metrics in the past to value your business or technology, or to help you make financial decisions. But how confident are you that you understand these metrics and know how and when to use them?

This blog post will provide a brief introduction to NPV and IRR and mention some advantages and disadvantages of each. You can learn a lot more about NPV, IRR, how to use them and related metrics like unacost, MIRR and EPVI (Excess Present Value Index) in the Moolman Institute Course Financial Modeling for Entrepreneurs 101: Master the Key Financial Concepts.

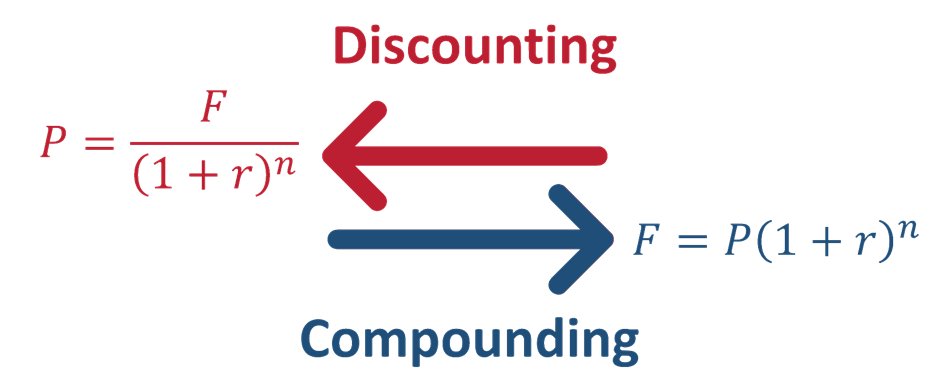

Money has a time value. The same amount of money is worth more in the present than in the future. To understand why this is so, imagine that you will receive $1 million at a specific date. There is a huge difference between that date being now or 40 years into the future. Until you receive the money, you cannot do anything with it.

Money has a time value. The same amount of money is worth more in the present than in the future. To understand why this is so, imagine that you will receive $1 million at a specific date. There is a huge difference between that date being now or 40 years into the future. Until you receive the money, you cannot do anything with it.

This is why money has a time value – because of the opportunity cost. Money in the present is worth more than the same amount of money in the future, because of its potential earning capacity. When you have the money, you can do things with it (such as investing it and earning a return).

Both NPV and IRR have advantages and disadvantages.

Both NPV and IRR have advantages and disadvantages.

Whilst NPV takes into account cost of capital, it is difficult to determine what rate you should use. Whilst IRR (as a percentage return) is more intuitive to understand, it cannot be used in all situations and can overstate returns.

Recent Comments